You build something people actually want, and then you hit the scary part: charging for it. Where does the money go? Who holds the card number? How do you take real payments without becoming a target or breaking a law you have never heard of? That wall stops more builders than any feature ever does.

In short, taking payments online means handing the dangerous part (the actual card details) to a trusted processor like Stripe, which charges the customer and pays out to you, so you never touch the sensitive numbers yourself. You are not building a bank. You are plugging into one.

Who actually handles the money?

Not you, and that is the whole trick. A payment processor (Stripe is the best known, and there are others) sits between your app and the card networks. When someone checks out, their card details go straight to the processor, never into your database. The processor charges the card, takes a small cut, and deposits the rest to you. You have seen this every time a checkout pops up that little secure card sheet or an Apple Pay prompt: that is the processor doing the part you never want to be responsible for.

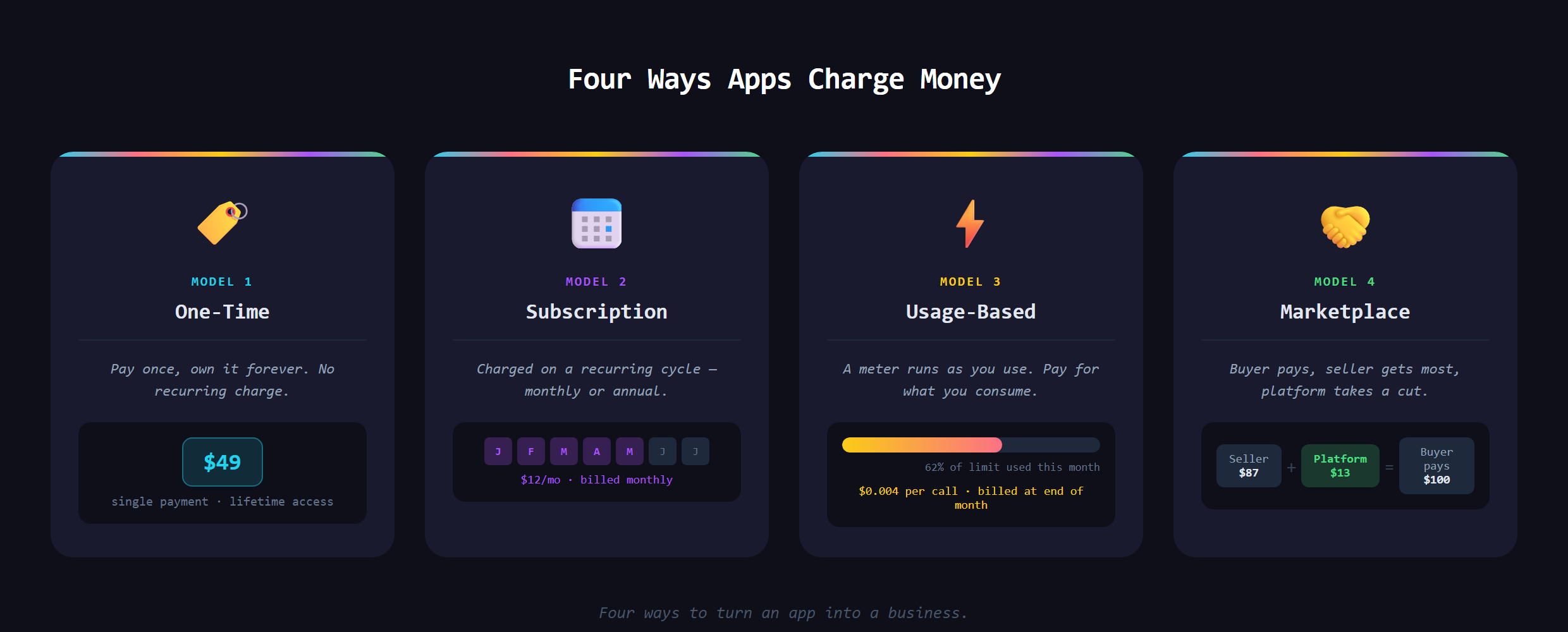

What are the four payment models?

Almost every app that makes money uses one of these four shapes:

- One-time: a single charge for a product or service. Simple and clean. Buy it, own it, done.

- Subscription: a recurring charge on a cycle, weekly, monthly, or yearly. This is how most software (including this one) is sold now.

- Usage-based: you pay for what you actually consume, like credits or metered API calls. Common with AI tools.

- Marketplace: a payment is split between a seller and the platform, which takes a cut in the middle. Think any app that connects buyers to sellers.

Plenty of products mix two, for example a subscription with usage-based overage. Knowing the four lets you pick the one that fits how your thing creates value.

What happens during a checkout?

The flow is more orderly than it feels. The customer enters their card with the processor, the processor confirms the charge went through, and then it quietly tells your app "this person paid." Your app hears that confirmation and unlocks whatever they bought. The important idea is that the money event and the access event are linked, so people only get what they actually paid for, and you have a clean record of it.

What else does a processor handle for you?

Charging the card is only the headline. A good processor quietly carries a pile of work you would otherwise have to build yourself: generating receipts, processing refunds, retrying a subscription when a card fails the first time, managing the whole lifecycle of a recurring plan, and flagging suspicious activity before it turns into fraud. Some even handle sales tax in the places that require it. This is the real reason plugging into one beats rolling your own. You are not just renting a card reader, you are renting an entire finance department that already knows the rules and keeps up with them so you do not have to.

What goes wrong if you do it wrong?

The mistakes here are expensive. Try to store card numbers yourself and you take on serious legal liability and become a juicy hacking target. Forget to handle failed renewals and your subscribers silently churn. Ignore chargebacks and refunds and your books turn into a mess. Worst of all, grant access before payment is truly confirmed and you give the product away. None of these are rare edge cases; they are the normal parts of charging money.

Why not roll your own?

Because handling real card data means meeting strict security standards, fighting fraud, and managing the whole messy lifecycle of a charge. It is a genuinely solved problem, and the solution is to plug into a processor and wire it in correctly. With an AI assistant in VS Code you can do exactly that, as long as you understand the models and the flow well enough to ask for the right one. That understanding is part of how Venom AI teaches you to Make Anything With AI.

Wiring real, secure payments into an app, and choosing the model that fits your product, is covered in Venom AI's Tier 2. The moment your app can take a payment, it stops being a project and starts being a business.